By

·

5 minute read

By

·

5 minute read

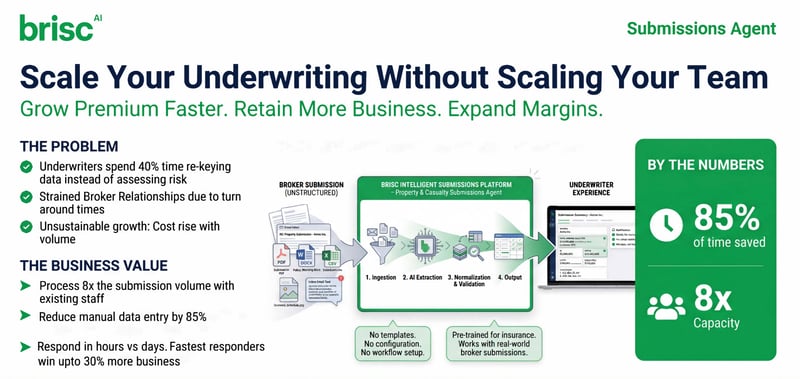

From intake to underwriting, see how Brisc AI processes broker submissions—extracting, validating, and delivering quote-ready data in minutes.

How does Brisc process broker submissions from intake to underwriting?

Brisc processes broker submissions by ingesting unstructured files such as emails, PDFs, Excel files, and SOVs, automatically extracting and validating underwriting data, prioritizing submissions, and delivering quote-ready data to underwriters.

The entire process works without portals, broker workflow changes, or heavy integrations — allowing insurance teams to move from submission to decision significantly faster.

As a result, underwriting teams using Brisc:

- Handle up to 8× more submissions with existing staff

- Move from submission to quote-ready in as little as 3 minutes (an ~85% reduction in preparation time)

- Respond to brokers in hours instead of days, improving service levels and competitiveness

Why do submission workflows break down for underwriting teams?

Traditionally, processing broker submissions requires manual intake and data entry that delays risk evaluation, quoting, and binding decisions.

In practice, most teams are dealing with the same realities:

- Rekeying errors slip into quotes. Data manually transferred from PDFs and emails contains mistakes. Wrong TIVs, missed locations, or transposed figures create E&O exposure and rework.

- Underwriters buried in data entry. High-cost talent spends hours copying information from submissions instead of analyzing risk and writing business.

- Broker relationships strained by delays.Turnaround times stretch to days. Brokers move urgent risks to competitors who respond faster.

- Promising submissions fall through the cracks. Without systematic tracking, submissions sit in inboxes. By the time you respond, the broker has already bound elsewhere.

Underwriters spend up to 40% of their time on non-underwriting tasks. McKinsey

The result is a process that looks manageable on paper but doesn’t scale.

This is the context in which Brisc operates — not as another system to manage, but as a way to remove friction from the very start of the workflow.

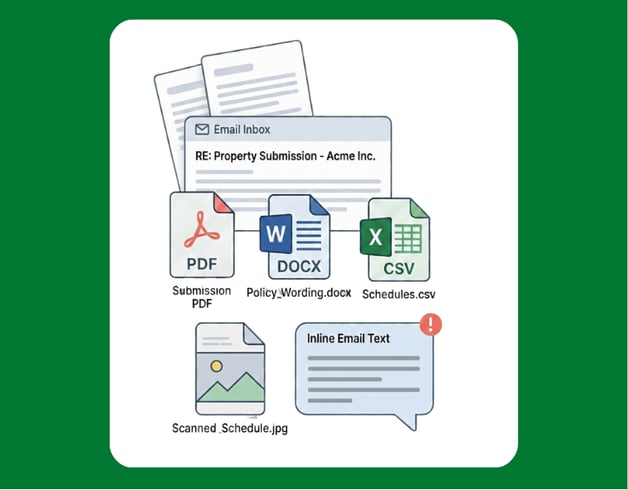

What happens when a broker submission enters Brisc?

When a submission enters Brisc, nothing about the broker or underwriting workflow needs to change.

Submissions are sent to Brisc’s Submissions Agent via email — exactly as they arrive today. There is no portal for brokers to learn, no new submission templates to enforce, and no upfront integration project required before value is delivered.

From the moment the submission is received, Brisc begins processing the full set of documents attached to it, capturing data from all associated emails, PDFs, Excel files, and SOVs.

This is where speed to market begins. By fitting into existing behavior instead of forcing operational change, Brisc removes the delays that usually occur before underwriting even starts.

What underwriting data does Brisc’s Submissions Agent extract?

Brisc’s Submissions Agent extracts underwriting-critical data directly from broker submissions.

.png?width=762&height=538&name=Brisc%20Blog%20Images%20(1).png)

The extraction process is domain-tuned for property and casualty underwriting, allowing Brisc to identify and capture the data underwriters actually need at intake without relying on fixed templates or standardized formats.

From each submission, Brisc extracts a broad set of underwriting fields, including:

- Insured entity details

- Location-level information

- Total Insured Value (TIV)

- Business Interruption (BI) exposures

- Limits and deductibles

- Coverage terms

These fields are captured consistently across documents, even when the same information appears in different formats, layouts, or attachments. Brisc is designed to work effectively across the wide variation typical in broker submissions.

In practice, this replaces the initial manual review that underwriters or analysts perform when opening a new submission — scanning documents, searching for key values, and assembling a baseline view of the risk. By extracting this information automatically, Brisc allows underwriting teams to begin evaluation immediately.

“The beauty of Brisc was taking about 80% of the manual labour away, so people can focus on underwriting instead of data entry.”

Nik Lucking, Managing Partner, Helix Underwriting Partners

How does Brisc normalize and validate underwriting data?

Brisc is pre-trained for insurance workflows, enabling it to evaluate underwriting data across emails, PDFs, Excel files, and SOVs as a single submission rather than as isolated documents. After extraction, Brisc reconciles information across all attachments to produce a consistent, underwriting-ready view of the risk.

As part of the normalization and validation process, Brisc:

- Aligns values that appear across multiple documents

- Identifies missing or incomplete information

- Flags conflicting data points between attachments

- Maintains traceability back to original source documents

This normalization ensures underwriting data is presented in a consistent format, even when brokers submit information using different layouts, terminology, or file types. Validation happens automatically and early in the process, bringing potential issues to the surface before underwriting decisions are made.

For underwriting teams, this removes a major source of rework and delay. Instead of discovering inconsistencies mid-review or during quoting, underwriters see data gaps and conflicts upfront — when they are fastest and least costly to resolve. The result is higher confidence in the submission and fewer interruptions once underwriting decisions are underway.

What does Brisc deliver to underwriters?

Brisc delivers quote-ready output that allows underwriters to begin evaluating risk immediately, without rekeying data or assembling context from multiple documents.

.png?width=800&height=565&name=Brisc%20Blog%20Images%20(2).png)

For underwriters, this includes:

- A consolidated submission summary covering key risk details, coverages, layers, and towers

- Structured underwriting data aligned to key fields and exposures

- Clearly flagged exceptions, gaps, or inconsistencies requiring review

- Direct traceability back to source documents for verification

Rather than reviewing raw emails and attachments, underwriters start with an organized, decision-ready view that reflects how they actually assess risk. The underlying documents remain accessible, but they no longer dictate the pace or order of review. Underwriters review structured, quote-ready data directly in Brisc and can then push it to their underwriting workbench with a single click.

This shifts the underwriting experience from preparation to evaluation. Time previously spent searching for values, reconciling documents, or clarifying inconsistencies is returned to underwriting judgment — enabling faster quoting, more consistent reviews, and higher throughput without increasing headcount.

How Brisc accelerates speed to market without heavy integration

Many in-market solutions fail not because of the technology itself, but because of how long they take to be implemented and adopted.

New portals, rigid data models, and deep system integrations can introduce months of lead time before underwriting teams see meaningful impact.

Adoption can become an additional hurdle when new tools require significant changes to established processes, slowing usage and delaying value even after implementation is complete.

Brisc is designed to avoid these delays by operating at the workflow layer rather than the system layer. Instead of forcing change upstream, Brisc fits directly into how underwriting teams already work.

As a result, Brisc can be deployed quickly and safely:

- Fast implementation: Most Brisc deployments go live within 2–6 weeks, without large IT projects

- No broker disruption: Brokers continue submitting via email and existing formats

- No intake portals: No new systems for brokers or underwriting teams to adopt

- No upfront standardization: Submissions do not need to be cleaned or templated in advance

- Minimal integration dependency: Core systems can be connected over time, not as a prerequisite

This approach allows underwriting teams to see impact early, while avoiding the operational risk and organizational drag that typically accompany automation initiatives.

By removing integration friction from the submission process, Brisc materially improves speed to market. New programs and lines of business can be supported immediately, without waiting for technical work to catch up. Underwriting organizations gain faster throughput and decision speed without introducing disruption or additional overhead.

What this enables for underwriting teams

By removing friction from submission intake and eliminating integration and adoption delays, Brisc’s Submissions Agent enables underwriting teams to operate with greater speed, consistency, and confidence — without changing how they work.

In practice, customers using Brisc see measurable improvements across the underwriting lifecycle:

- Increased underwriting capacity: Teams are able to handle up to 8× more submission volume with existing staff, by eliminating manual intake and preparation work.

- Faster time to quote-ready: Submissions can move from intake to a quote-ready state in as little as 3 minutes, an ~85% reduction in preparation time.

- Improved broker responsiveness: Underwriters can respond to brokers in hours instead of days, improving service levels and competitiveness without added effort.

- More consistent underwriting decisions: Standardized, validated submission data reduces variability and late-stage surprises.

For underwriting organizations, these gains compound over time. As submission volume grows, Brisc allows teams to scale efficiently, launch new programs faster, and maintain underwriting discipline — without increasing headcount or introducing operational complexity.

See Brisc in Action

Experience how Brisc’s Submissions Agent transforms unstructured broker submissions into quote-ready data in minutes — without changing how your team works.

Forward a sample submission and see the results for yourself, or book a demo today.

FAQs

Does Brisc AI require brokers to change how they submit risks?

No. Brokers continue submitting risks via email using their existing formats. Brisc ingests submissions exactly as they arrive, without portals, templates, or workflow changes.

Does Brisc require deep system integrations to deliver value?

No. Brisc operates at the workflow layer and does not require heavy upfront integrations. Most customers are live within 2–6 weeks, with optional system integrations added over time.

What types of files can Brisc process?

Brisc processes common submission formats including emails, PDFs, Excel files, and statements of values (SOVs), treating all attachments as part of a single underwriting workflow.

How quickly can underwriters start working a submission in Brisc?

Submissions can move from intake to a quote-ready state in as little as 3 minutes, depending on submission complexity and completeness.

What underwriting data does Brisc extract from submissions?

Brisc extracts underwriting-critical data such as insured details, location information, Total Insured Value (TIV), Business Interruption exposures, limits, deductibles, and coverage terms.

How does Brisc handle missing or conflicting data?

Brisc automatically flags missing, incomplete, or conflicting information during validation and surfaces these issues early, with traceability back to the original source documents.